Five Below: the odd one out within the retail industry

Five Below: the odd one out within the retail industry

The retail industry has conventionally been a rather stable industry; a low growth industry, lacking the “sexy” tailwinds as compared to its tech counterparts. While conventional wisdom has its truths, there are actually multiple pockets of opportunities within the space, with interesting dynamics. In comes Five Below.

The essay is divided into 5 main sections:

1. Overview of Five Below

2. Setup of the stock today

3. Key investment thesis for Five Below

4. Valuation and return profile

5. Risks to the investment

Background of Five Below

Five Below is a discount retailer operating primarily in the US, offering, trendy products mostly priced at $5 or below that are primarily targeted for tweens and teens (to be detailed further later). The company was established in 2002 and has expanded significantly over the years across the US. Today, the business operates 1,403 stores across the US and generates approximately USD3.1bn in sales over the past 12 months. From 2017 to 2022, Five Below has grown its revenue at an impressive 19% CAGR, while growing its store count at a staggering 16% CAGR. The residual growth of ~3%, would primarily come from better comparable sales (same store sales growth).

Source: Annual reports

Today, Five Below offers more than 4,000 SKUs, primarily in 3 categories, which are Leisure, Fashion & Home and also Snacks and Seasonal. While these are the 3 broad categories of the merchandises that are reported, Five Below separates its merchandises further into 8 distinct “Worlds”.

Source: Annual report

Further analysis on Five Below indicate 3 primary differences between Five Below relative to other competitors:

The first primary difference is the trend-right products that they focus to sell instead of generic, staple products that are typically sold. i.e. non-trendy, products that are used in everyday lives such as food, toiletries etc.

The second difference is that consumables represent a lower contribution to sales relative to other discount retailers / retailers. Five Below only sells certain snacks and candies rather than grocery related items. This indicates that they may have lower product velocity compared to other retailers. See picture below for reference, with average transaction frequency of Five Below being lower than other discount retailers based on publicly available data by Second Measure.

Source: Bloomberg Second Measure

The third difference is that Five Below’s products are very focused on teens and tweens, essentially products that are more geared towards brining fun and enjoyment instead of products that are critical for human sustenance (such as food and toiletries).

Five Below’s business model is relatively simple, with revenue primarily derived from merchandise sales in stores, while online sales represent a smaller contribution of overall sales (estimated at <5% of overall sales). This is very different relative to other retailers that generate and place higher emphasis on online sales (to be discussed further later).

Setup of the stock price today

Despite meeting expectations, Five Below’s share price dropped after its 2nd quarter earnings announcement. The company reported financial results for the fiscal second quarter of 2023 on Aug. 30. Q2 net sales of $759 million and net income of $46.8 million were both within management's guidance, and management maintained guidance for revenue. Nonetheless, the company lowered its guidance for net income from $297-$319 million to $295-$311 million, a 2% drop in guidance. The drop in net income is primarily driven by higher shrinkage reserves as the theft is becoming a more prevalent issue, not just for Five Below but across the retail industry. While they expect some gross margin leverage from lower freight cost, the increase in shrink reserves is expected to offset this. On top of that, SG&A is expected to increase as % of revenue due to one-time cost management and normalized incentive compensation. The positive thing to note is that management is being very proactive in dealing with the shrinkage issue and has been conducing a large-scale audit and cost management plan to deal with shrinkage, including reviewing self-checkout rollouts across its stores. While the drop in operating income margin guidance can be viewed as a negative, personally, I believe this is a short blip in the stock price and represents a compelling risk-reward for investors as a long-term opportunity.

Based on a reverse DCF on Five Below, price today at ~$180 implies that Five Below is able to grow its store count at the rate guided by management with comparable sales growth expected to be around 3% on average (implying average sales per store to grow around 2-3%) up to 2030. On the margins side, operating margin is expected to reach 15% in 2030, with terminal growth to be at 3% and discounted at 9.2%

Source: own estimates (as of 20 November)

Today the stock is trading at ~30 EV/EBIT, a discount relative to its 5-year historical average of (37.8 EV EBIT). Meanwhile, consensus estimates are showing that operating margins to reach ~12% by 2026, with sales at ~$4.9bn with an average target price of $212, an upside of ~17% from today’s share price.

Source: MarketScreener (as of 20 November 2023)

Primary Investment Thesis

There are 4 key points underpinning the thesis for Five Below:

Five Below operates in a very attractive subsegment within the retail industry, underpinned by strong tailwinds in consumer discretionary spending preference with attractive industry dynamics, coupled with differentiation against other conventional dollar stores and retailers

Five Below is an attractive asset to own, given its differentiated value proposition, industry leading 4-wall EBITDA margin, driven by strong execution in merchandizing, real estate strategy and sourcing. It has generated strong comparable sales over the years, despite its unconventional product offerings, tapping into an untapped customer segment with high purchasing power for the products that they offer. While its existing business is attractive, it has a strong growth runway, underpinned by store expansion, conversions and multiple other value levers to drive both sales and margin expansion

Five Below is undervalued relative to its past 5 year EV/EBIT multiple. A DCF valuation with conservative assumptions on growth, margins and FCF generation and multiple yields a share price of USD 357, after taking into account potential stock dilution, and generates an approximately 100% return to investors over 3-year period.

The risks to the business coming from other retailers, other e-commerce players and its target customer segment is relatively insulated, given the dynamics of the industry, Five Below’s management is already addressing some of the concerns from other competitors

Attractive subsegment of the retail industry

From an industry standpoint, a simplistic view of Five Below would suggest that it operates within the discount retail industry. Nonetheless, there are some nuances between Five Below against other discount retailers such as Dollar Tree and Dollar General in terms of the customer segments that they target and their product offerings. I believe that its worth exploring some of the similarities between Five Below and other discount retailers and what separates them.

In terms of similarities, at its most fundamental level, all discount retailers, including Five Below offer 2 very compelling value proposition to its customers, which is price/value and convenience, respectively.

Source: Statista

Based on multiple consumer studies / surveys, price / value remains one of the key reasons people shop at dollar stores / discount retailers. Discount retailers are able to provide everyday items to consumers at very cheap prices, relative to convenience stores or big-box retailers such as Walmart and Target. Based on a Morning Consult Survey in June 20234, dollar stores are becoming a shopping destination across all income groups, including wealthy households. Similarly, across all generations, consumers are looking to “trade down” and seek more value in their purchases based on a McKinsey study earlier this year.

Note: Data for Dollar general, Dollar Tree and Family Dollar. Figures for June 2023 run to the 12th. Source: Monthly rollup of daily Morning Consult Brand Intelligence surveys, most recent of 1,553 US adults conducted June 1-12; approximate error +/-2.49 pct. Pts; McKinsey Customer Survey 2023

Part of this movement is indubitably due to the tightening macroeconomic conditions, with relatively high inflation in recent months and higher interest rates. It should be noted, however that this movement is not a recent phenomenon, as evidenced by the strong same store sales / comparable sales growth seen in discount retailers relative to big-box retailers and GDP growth over the past decade. Nonetheless, contributing towards this movement of “trading down” is also driven by social media influence/changing consumer behavior, which has been widely promoted by social media influencers in recent years. Videos tagged #dollartree have a combined 7.6 billion views on TikTok with many featuring influencers trying out what are known as dupes of popular high-end beauty products and other goods. On the other hand, there has been a shift in consumer behavior to becoming more value conscious5. Consumers are shopping more often with smaller baskets, which gels well with discount retailers’ smaller SKU assortment and store size. In addition, discount retailers typically price lower than the mom & pop convenience stores, as well, which leaves them as the primary destination for consumers. Given all these dynamics, discount retailers are the best option for consumers relative to its substitutes i.e. big box retailers and convenience stores.

Note: SSSG = Same Store Sales Growth | Source: Company annual report, Government data

“Consumers are shopping a little differently now. They are shopping a little more often and perhaps picking up slightly smaller baskets.” 5

David Gordon, research director at Edge by Ascential.

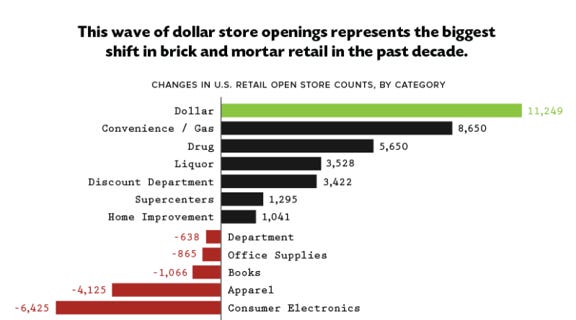

Convenience is also a primary reason why discount retailers are highly preferred by consumers relative to its big-box counterparts and convenience stores. There are a few lenses to consider that contribute towards the higher convenience seen in dollar stores relative to its big box counterparts. The first is the relative abundance of the stores relative to big-box retailers within a given population. To give a sense of scale, dollar stores outnumber Walmart and Target by a scale of 7:1 and 18:1, respectively. Over the past decade, dollar stores have outpaced any other retail store openings by a significant margin. This increases the coverage of dollar stores, particularly in rural areas, where there are very limited alternatives (Dollar General specifically expanded in rural areas in order to capture this demand). Increasing store density per population reduces the time taken to get to the store, which ultimately improves accessibility to consumers.

Source: Nielsen

The second lens on convenience is the size and design of the stores itself. Typically, dollar stores have an average size between 7,000 sqft to 9,000 sqft, relative to its big-box counterparts, which typically have much larger retail square space per store (Target at ~140k sqft). A lower store size ensures that customers are able to easily navigate within the store, with smaller parking areas, to ensure a seamless and quick shopping experience. This is further aided with a relatively simple store design and layout. What is interesting, is also the fact that these store experiences also induce customers to “treasure hunt” in the store to find the best bargains (these small “wins” are a lot of times shared on social media, which further increases customer traffic). These dynamics apply to Five Below as well despite its different product assortments.

Source: Company annual reports

A final interesting point to note is that, despite the trading down movement, consumers are still willing to splurge, with 40% of consumers in the McKinsey survey indicating that they are eager to spend in the coming year, particularly younger demographics. This would very well benefit Five Below, given its target demographic and is a perfect segue to understand the differences between Five Below and other discount retailers in terms of the market that they compete in, which is one of the primary differences between Five Below. There are 2 primary difference that I think is worth highlighting from a market perspective on how Five below is different: i) Its target customer segment, ii) Primary products that they sell in their stores.

Source: McKinsey

One of the interesting things I find about Five Below is their singular focus on targeting the teens and tweens segment, defined by the company as Gen Z (aged between 8-14 years old) and their parents, which are defined by Five Below as Gen X / Millennial (aged between 24 and 45 years old) across all income segments. Given this very specific target segment, compared to its discount retailer counterparts, who target across various demographics, we would need to understand how this segment is expected to grow going forward and what are the tailwinds behind this customer segment that make Five Below an attractive investment.

Based on data from the US Census, this age group represents 24% of the US population as of 2022 and is expected to grow over the foreseeable future, albeit at a slow rate of around 0.26% to 2030 due to declining birthrates in the US. This ensures a healthy supply of new cohorts for Five Below to continue to penetrate and win. Aside from the demographic tailwind, Gen Z’s consumer behavior also benefits Five Below. Based on the survey conducted by the International Council of Shopping Centers (ICSC) in 2023, Gen Z consumers are highly cost conscious and lean towards discount destinations. While there are many factors contributing towards this, one that I find rather compelling is the fact that they are age having experienced 2 major economic crises, in 2008 and also in 2020, following Covid. These events have likely shaped their experiences and their attitude towards more prudent financial decision making.

Source: ICSC Gen Z Survey7

While Gen Z’s are considered a digital native cohort, having grown up in an era of ubiquitous technological innovation, that are have been made accessible to the masses, it is surprising to see that they 55%8 (based on survey Redpoint Ventures) of them still prefer in-store shopping. Nonetheless, online channels have become more popular (growing 20% since 2020), suggesting that online shopping habits from the Covid crisis is here to stay. That being said, there are multitudes of reasons as to why in-store shopping still remains supreme, with the primary reason being convenience (i.e. to get items immediately and also to test and try), both factors gelling well with the primary principles / foundations of Five Below’s store layout and design. Five Below explicitly densifies its stores, so that its highly accessible to consumers, and also allows for customers to try their products in store, emulating a ‘treasure hunt’ experience, which is highly engaging for its customers (i.e. kids). These factors make targeting this customer segment highly compelling, and are tailwinds for Five Below

Source: ICSC Gen Z Survey7

The second primary difference on Five Below compared to its discount retailer counterparts, which is mostly discretionary items rather than consumables. While Five Below does not explicitly detail out what portion does consumables make up as % of revenue, it does report its Snacks and Party segment, which makes up about 23% of its business in 2022 and has been growing substantially over the years at a 29% CAGR since 2018. While consumables contribution has grown over the years, this revenue contribution differs significantly from Dollar General and Dollar Tree (including Family Dollar) that generate 80% and 61%, respectively from consumables in the last 12 months. The question then is, are the product assortments sold by Five Below able to benefit from the trading down trend that we see over the past years? I believe the answer is Yes, as proven by Five Below’s average comparable sales over the past decade, being higher than the other players. To further reinforce this view, I looked at macroeconomic data from the US Census and found out that the percent of disposable income spent on “Toys, hobbies, and playground equipment” (a reasonable proxy for demand of Five Below’s products) has been stable over the years. In general, the US population spends around 0.2% of their disposable income on such items since 2015 to 2022, which suggests that there is constant demand for such products (an increasing in dollar terms given the natural rise in annual income year by year) and I believe this will continue to be the case as children (and even adults increasingly) still need various forms of entertainment, not just digital entertainment (despite the rise in VR/AR). On top of that, based on data from Greenlight, the average weekly allowance for kids (below 19 years old) have been above $5 in 2023, with average weekly allowance for 5-year-olds at $6.04 while 18-year-olds earn around $29.69, which implies that kids today are capable of purchasing items in Five Below.

In summary there are 4 key industry tailwinds at play, both that affect other discount retailers and also those that are more idiosyncratic to Five Below:

1. Macro tailwinds

Consumers are increasingly trading down their spending from Big Box retailers to discount retailers due to better value for money

Demand for discount retailers is expected to grow going forward driven by higher levels of convenience, due to ubiquity of store location as well as convenient store design and layout

2. Idiosyncratic tailwinds

Gen Z is an attractive customer segment to target, given their preference for value, their demand for engaging store experience as well as structural demographic growth

Demand for non-consumables is expected to remain in the foreseeable future

With all these industry dynamics at play, I believe that Five Below’s is well positioned to capture them in the coming years.

Strong growth prospects supported by attractive business fundamentals

Aside from industry tailwinds, there are 3 asset-specific factors that make Five Below an attractive investment:

Strong growth prospects with top-line drivers pointing positively and is expected to drive 19% CAGR over the next few years, driven by store expansion and comparable sales / same store sales growth (through store conversions)

Attractive 4-wall EBITDA margin with industry-leading payback period. Its existing operations are one to emulate and envy. Operating leverage is top of mind for management, with potential to achieve long-term operating margin of 14%, driven by scale, normalization of incentive compensation and marketing

Additional value creation levers / catalysts by management, contributing to SSGS, :

Investing in omnichannel

Loyalty program

1.1 Robust store expansion plans

Five Below in my opinion has a well thought-out long-term strategy for value creation, focused on 5 key pillars with the ultimate ambition of achieving its “triple-double” goal of tripling US store count and doubling topline and bottom line by 2030. These 5 pillars are:

The first 2 pillars are essentially the key drivers of revenue growth which are number of store growth and average sales per store growth, respectively . Based on the management’s plan, Five Below is expected to expand its store footprint to 3,500 by 2030, growing at an estimated 16% CAGR (Historically, they have grown at 17% since 2015. This store count growth is in line with other discount retailers, which have been expanding aggressively as well, particularly Dollar General. Given the trading down movement that we have seen, I am happy to underwrite this level of store growth in my assumptions (discussed later), which will drive revenue growth.

The flipside of this expansion is the ability to utilize the incremental operating leverage that scale provides. Through its densification strategy in key markets, Five Below will be able to expand its margins, through lower marketing, distribution and operating costs. I expect incremental margin improvements, converging towards Dollarama, a leading discount retailer in Canada, in the best case scenario. I believe the shrinkage issue that they are facing is temporary and margins should continue to expand in the coming years. Meanwhile, freight cost is also expected to normalize, which will drive margins higher as well.

1.2 Continued store conversions

Five Beyond is currently in the process of converting its existing stores. As of Q2 2023, they have converted over 600 stores with 250 being completed at the end of 2022 (20% of their store fleet at the time). That being said, around 50% of their existing stores (as of 2022) have yet to be converted into their Five Beyond prototype, which suggests a high runway for growth. Based on the recent Q2 call, converted stores are able to achieve mid-single digit uplifts in comparable sales, both from average basket size (~2x basket size) and also in terms of higher units per transactions (+50%).

“Yes Paul. I mean, look, nothing's changed on the conversion stores. We're still seeing mid-single-digit lift with transactions being even higher than that in converted stores. So really, I mean, we are uber excited and standing behind this conversion strategy. We've got the 400 that we've done this year and expect to get right back after that again next year with some more stores. But that mid-single-digit lift is consistent with what we saw at the end of last year and are continuing to see this year year-to-date.”

Joel Anderson, CEO of Five Below, Q2 2023 earnings call

Five Beyond offers products that are prized above the typical $5 (typically in the range of $5 to 10$, still far below the average price), and consists of up-leveled products such as licensed products like the Hello Kitty Funko or a basketball arcade set. There are no specific categories of the products, just that they are higher priced that is accompanied by generally higher quality and higher functionality. In addition to product extensions, the store format was also redesigned to ensure an “easy-in, sticky-out” format to ensure customers spend more time to purchase things in the store. The extended product offerings also expands the addressable customer that goes to Five Below, given that the products cater to a wider audience (i.e. higher earners). Due to these store conversions, average sales per store is expected to expand going forward. Five Below is already seeing benefits from these conversions and store expansion as shown below9 wither higher brand traffic growth. They have been able to do this consistently historically as well (no breakdown in 2020 and 2021).

Source: Gravy Analytics

Note: No breakdown for comparable sales in 2020 and 2021 | Source: Company annual report

2.1 Attractive Underlying Business

While growth prospects are certainly there, the underlying business itself is highly attractive. Five Below has one of the industry’s leading investment payback period for a new store of less than 1 year, with an impressive 4-wall EBITDA margin of 25%. Over the years, through various prototyping of new store formats, the company has been able to drive EBITDA margin expansion as well as higher average sales per store.

Source: Investor presentation

In addition to the introduction of new store formats, its merchandising strategy and real estate strategy also contribute towards expanding topline and margins. Key to its success in merchandising is the battle-tested playbook that they employ to determine what products to place on their shelves The establishment of the company's eight distinct merchandise categories serves as a structured platform for efficiently detecting emerging trends within these domains. By honing in on these eight principal categories as opposed to diversifying excessively, the firm can strategically allocate resources to ensure accurate trend forecasting. Five Below has institutionalized a methodical process for trend identification, underscored by a consistent presence of buyers in the market and an active feedback loop with store managers, who engage directly with consumers. This real-time feedback is channeled to the procurement team. Upon identification of a potential trend, Five Below’s agile operational model facilitates a rapid product lifecycle, translating a concept into an in-store product in a timeline of six weeks or fewer. This is exemplified in recent quarters, where they capitalized on the Barbie and Super Mario trends, by ordering related merchandises into stores. Principally, the key to successful merchandising boils down Five Below’s ability to provide significant value to customers despite the fact that customers are essentially purchasing products that are not necessities.

“Many of Five Below’s items are a cocktail of functionality and kitsch — such as light-up Bluetooth speakers, cute makeup pouches and quirky cellphone accessories. It’s a shrewd approach, given that consumers don’t like to spend money unnecessarily but still want to indulge,”

“Guilt is not necessarily something that people are conscious of, but it still drives their behavior,” Kivetz said. “So the ability to match in the same item a sense of luxury and necessity, it helps alleviate the guilt and helps make the purchase much easier,” he said. “And when the cost is already low . . . it’s very clever merchandising on Five Below’s part.”

Ran Kivetz, a professor of marketing at Columbia Business School who has studied how emotions shape consumer behavior for more than 25 years.

Being trend right is critical for the business, given that i) Five Below targets a customer segment that are very trend-sensitive, ii) Five Below does not have products that are “stable” in demand (i.e. grocery items e.g. food etc) unlike its dollar store counterparts except for its snacks segment, which are mostly candies (non-essential). Given this product orientation, being right on trend ensures that customers are enticed to spend in Five Below. While its product offerings are differentiated, fundamentally, it is still consistent with merchandising principles that make dollar stores a successful business, which is limited SKUs (Five Below has ~4k SKUs, Dollar Tree has ~7.6k to 8k, Dollar General, ~10k while Walmart and Target have ~140k and ~80k, respectively). This concentration of SKU benefits Five Below in terms of better focus on products that are trend-right, streamlined inventory management, reduced staffing needs (given less time needed for organizing and stocking goods), lower storage needs / space required as well as lower COGS, given that they can negotiate better terms through larger orders of fewer item. Lower SKUs is also needed given that store sizes are small (similar to other discount retailers), and hence they need to maximize their real estate dedicated to shelf and merchandising, rather than storage.

Given the firm’s large emphasis on growing store counts to drives sales, it is also imperative to understand the firm’s real estate and store design strategy, which is a differentiating factor for Five Below as well. Underpinning its real estate strategy are 3 different segmentations of retail spaces that benefit from high customer traffic (power1, lifestyle2 and community3), coupled with 3 main locations of stores (urban, suburban and rural). The focus on high-traffic retail venues complements their strategy perfectly, given that the products that they sell targets teens and tweens, consumers which are more likely to spend more time in malls or more dense retail venues. Establishing stores in these areas ensures that Five Below not only benefits from high-customer traffic but also improved brand awareness and consequently better store economics.

Historically, the firm has focused on opening stores in suburban areas within the 3 retail spaces highlighted. Nonetheless, the firm has shifted its focus and will be opening more stores across urban and rural areas as well. All of its stores are currently leased, which reduces CAPEX requirement, with majority of them having a 10-year initial term, with option to extend. Once the firm has identified an attractive market to expand into, Five Below’s strategy is to then densifiy the market by establishing clusters of stores, given the scale benefits that they can derive from market concentration i.e. lower marketing cost, lower distribution cost, higher brand awareness etc. This is extremely beneficial to the firm, as it focuses on landing and expanding in attractive markets rather than expanding its stores across different geographies, without building core presence in any. This store clustering strategy does not just stop at the point of identification of location but also in store openings as well. Five Below would open multiple stores in a single market on the same day, enabling them to leverage marketing and pre-opening expenses and generate initial new market brand awareness.

Source: Investor presentation

Its store designs are also significantly different from competitors. Stores are designed to ensure customers have a fun experience, with shelves being less than 5 feet tall to ensure customers are able to have sight-lines across the store, coupled with distinctive merchandise fixtures and colorful signage to convey their value proposition and encourage customers to spend.

As a result of its successful merchandising strategy and real estate strategy, its stores are able to generate approximately $2 million in the first full year of operation with an average new store cash investment of approximately $0.4 million (figure includes store build out net of tenant allowance, inventory net of payables and cash pre-opening expenses). This allows its stores to achieve a 25% EBITDA margin with a payback period of less than 1 year. This is also reflected in the average basket size of customers relative to competitors.

Source: Bloomberg Second Measure

3.1 Omnichannel experience as additional value lever

There are also additional value creation levers for Five Below, which are omnichannel experience and also the loyalty program.

Interestingly, online sales make up only a small portion of the business, and it seems like management is not too worried about it, given the small contribution. In the Q2 earnings call, he mentioned that the business is relatively insulated from the online retailers like Amazon, just due to the fact that online sales make up a very small portion of revenue (<5% of the business).

“Yes. Look, online has been good for us. Just to remind everybody, it is low single-digit of our total business, which is a very different profile from everybody else. And certainly, what insulates it is it's a small piece of the business, for starters. So, even if it had a material impact, it's a very small impact on our total business.

Joel Anderson, CEO of Five Below, Q2 2023 earnings call

While it does seem management’s comments are downplaying the significance of online operations, management did mention that online has been good for them in terms of getting an early read on customers, which would help them in creating the right merchandising strategy at any given moment. With the agility that they need from trend identification to sourcing and merchandising, online channel will continue to strengthen this great advantage that they have.

“We already have a good sense of what's going to sell in Halloween here because it's been online for about four weeks now. And we do that every -- with every seasonal change, we get it up online first and it more helps us prepare and set the stores. But no impact from -- that we can tell from pure online retailers. Thanks.”

Joel Anderson, CEO of Five Below, Q2 2023 earnings call

I believe that omnichannel experience will be critical going forward and will increasingly garner more attention from management. As assessed earlier, online channels is growing substantially and will is expected to continue given Gen Z’s preference. This leaves a lot of white space for Five Below to continue to invest in e-commerce and drive further penetration in online commerce. While a higher contribution of online sales leaves it more vulnerable to competition with online retailers, I believe that the growth and establishment of an omnichannel experience will create incremental value to the business.

3.2 Introduction of loyalty program

The final thing to add is the introduction of a loyalty program to its customers, which is expected to be implemented in 2025. While the announcement is not new, I believe that investors are underestimating the impact of loyalty programs for a retailer and not fully baking in the uplift in sales and margins from the loyalty program10. Nonetheless, the deployment of this loyalty program would need to be underpinned by strong elements of personalization, which is key to driving better retention and ultimately sales.

Valuation

Based on my assessment of Five Below, I believe that sales and margin expansion are able to happen faster than consensus estimates, driven by further operating leverage, and pricing ability of Five Below due to further store conversion. The introduction of the loyalty program should also drive further margin expansion, from purchase of higher margin goods. I am also expecting marketing expenses to normalize and be able to experience better operating leverage. As such, I am valuing the company at a conservative EV/EBIT of 26 at FY26, due to multiple compression across markets (average 5-year EV/EBIT was 36), with sales at $5.8bn and operating margin at 14%, closer to management’s target and converging to Dollarama’s operating margin at ~23%. Dollarama is a leading dollar store player in Canada, which I believe is one of the best in class dollar store player in North America. Based on these assumptions, I have arrived a price target of $357 by FY26, an approximately 100% return from today’s share price.

Source: Own estimates

Key Risks

That being said, these forecasts above are more optimistic than others, but I do believe in management’s ability to execute, as they have done over the years. The recent blip in guidance presents a great opportunity for investors. Key risks to look out for Five Below:

1. Execution risk

2. Risk of targeting teens and tweens

3. Risk of the business from other retailers

4. Risk of the business from online retailers

Execution risks remain with the ability of Five Below to execute effectively on several fronts including, identifying key trends that are relevant to teens and tweens, drive operating leverage given expansion in scale, and continue to innovate. Nonetheless, management has always demonstrated the ability to execute, as shown by their impressive historical performance. Operating margins should be able to expand with the introduction of Five Above, increasing the average basket size and higher priced (and margin) products and expanding stores should allow Five Below to generate further economies of scale.

Some are also suggesting that targeting teens can also be risky, given that this is a very specific customer segment. There’s a few reasons why I believe, this is already in the works to be mitigated by management. The first is the introduction of Five Below, which extends products to include tech accessories and other products that are more friendly for a wider range of customers. In addition, they are also introducing products that caters to this segment as they grow up, including ear piercings, personalized car accessories and many others. Products are also more ESG friendly today, which bodes well with preferences of Gen Zs

Source: McKinsey

There are also potential risks from other retailers, given that barrier to target teens and tweens are not that high and products can be sourced, relatively easily. Nonetheless, there are some limitations for this to happen effectively, given the significant difference in strategy relative to other discount and big box retailers. Other discount retailers and big box retailers are focused on targeting a wider target segment, with stores being designed to manage a wider target segment, instead of being targeted for teens and tweens. In addition, the product mix across retailers are significantly different from Five Below, with the former skewing more towards consumables and I don’t believe this would change anytime soon.

The last risk is the risk from online retailers such as Amazon. Key risk is that product discovery today, largely starts from Amazon and Google, which is a risk for Five Below. However, thinking about the dynamic of online sales and the customer journey of online shoppers, they typically know what they want or are searching for. The beauty of Five Below is that shoppers are buying for the sake of discovering new products that they have never thought they wanted. In addition, as stated before, online sales represent only a small portion of the business and shouldn’t pose much threat to Five Below. But nonetheless, given the importance of omnichannel, management is already ramping up investments in digital sales, and I believe this should help alleviate some of the concerns from online retailers.

Conclusion

I believe that Five Below represents an attractive opportunity, with the ability to generate 100% returns in 3 years. There are a lot of macro tailwinds that will help drive growth for the company and there are a lot interesting idiosyncratic factors that ensure Five Below is able to capitalize on these macro factors and generate substantial value for shareholders. Ahead of its 3rd quarter earnings, it will be interesting to see if there are any changes to the company’s guidance for the year and also if they can provide more color on FY2024, particularly on margins and operating leverage.

Disclaimer - This article is not advice to buy or sell the mentioned securities, it is purely for informational purposes. While I’ve aimed to use accurate and reliable information in writing this, it cannot be guaranteed that all information used is of such nature. The views expressed in this article may change over time without giving notice. The mentioned securities’ future performances remain uncertain, with both upside as well as downside scenarios possible. Before making any investment, it is recommended to speak to a financial adviser who can take into account your personal risk profile.

References

1“Power” shopping center to refer to an unenclosed shopping center with 250,000 to 750,000 square feet of gross leasable area that contains three or more “big box” retailers (large retailers with floor space over 50,000 square feet) and various smaller retailers with a common parking area shared by the retailers.

2“Lifestyle” shopping center to refer to a shopping center or commercial development that is often located in suburban areas and combines the traditional retail functions of a shopping mall with leisure amenities oriented towards upscale consumers.

3“Community” shopping center to refer to a shopping area designed to serve a trade area of 40,000 to 150,000 people where the lead tenant is a variety discount, junior department store and/or supermarket

4https://kanebridgenews.com/one-percenters-keep-shopping-at-the-dollar-store/

6https://www.statista.com/statistics/1304255/dollar-store-reasons-to-shop-us/#:~:text=Perhaps%20unsurprisingly%2C%20the%20top%20reason,people%20enjoy%20browsing%20the%20stores.

7 https://www.icsc.com/uploads/about/2023ICSC_Gen_Z_Report.pdf

8 https://www.redpoint.com/start/written/tea-on-genz/

9 https://gravyanalytics.com/blog/dollar-store-phenomenon-foot-traffic-consumer-behavior-2023/

10https://www.forbes.com/sites/forbesagencycouncil/2020/01/29/the-value-of-investing-in-loyal-customers/?sh=712ec50021f6

11https://greenlight.com/blog/average-allowance-by-age-for-kids-2022

Great write-up! I really appreciated how you highlighted the similarities between Five Below and other discount retailers like Dollar Tree and Dollar General, as well as what sets them apart.