Trade Desk, a crown jewel for distributing digital ads on the open internet

Trade Desk, a crown jewel for distributing digital ads on the open internet

Disclaimer: I would like to apologize for the sheer length of this post. I view this as a form of learning for me to synthesize what I have learned so far on the industry and the company. Please skip certain sections if you are already familiar with the industry or company.

I have always been intrigued by the advertising market, not just because of its sheer size but also because how many tech companies rely on it as a source of revenue. The advertising market has evolved significantly over the decades from linear TV, to the proliferation of the internet and social media platforms to connected TVs (CTV) today. While there are many facades to advertising, at the risk of stating the obvious, advertising today is increasingly digital and it is safe to assume that in the future, all advertisements will be digital. As this unfolds, there will be companies that will indubitably benefit from this shift such as your Google, Meta, Amazon and all the other digital advertising giants out there. But I guess, the work to be done here is discerning where the highest upside or alpha can be generated. This led me to researching on the various players in the advertising value chain and why I believe Trade Desk offers a great risk reward.

This essay will be divided into 5 main components:

A primer on the online advertising market and the potential growth of the segments (you can skip this if you’re already familiar)

A background on Trade Desk

Setup of the stock today

Primary investment thesis for Trade Desk

Valuation and Risks

Overview of the online advertising ecosystem (Programmatic buying)

The online advertising market is without a doubt a complex industry to understand, one that I myself am in no way expert in. So here my attempt to distil my learnings of this industry. Forgive me for butchering anything or missing out anything, but this is I believe a sufficient primer for those who wish to understand key building blocks of the advertising market. There are multiple layers to the advertising market, but I believe at the highest level it is useful to discern what are walled gardens vs open internet advertising. Walled garden refers to the closed advertising ecosystem provided by some of the large tech companies today such as Google, Meta (Facebook and Instagram) and Amazon. They essentially maintain their own ad inventory, they facilitate purchase and selling of ads within their applications / ecosystems, essentially end-to-end control over advertising within their ecosystem and operates independently with limited transparency to outsiders and even advertisers. On the other hand, the open internet refers to anything outside of the walled garden players, essentially publicly accessible and not restricted by any platform’s specific control, which allows for interoperability between different technologies. Think of the websites such as Wall Street Journal or Instacart’s platform.

The next level refers to the mode of purchase for online advertisements. Fundamentally, ads can be purchased either directly or programmatically. Direct purchase implies that advertisers or ad agencies working directly with a publisher or social media platform, negotiating prices, placement of ads, dates and how long it would last. Programmatic, on the other hand, is the automated process of buying and selling advertising space in real-time (i.e. Real Time Bidding – RTB), typically done through an ad platform (applies to both walled garden and open internet players).

Now that we have the layers described, we can move on to the actual value chain of digital ad purchases, with a focus on open internet ad market, as this is where Trade Desk operates. Below is my attempt of a visual representation of the digital advertising ecosystem. I understand that there are more interdependencies between the players but this is directionally correct to understand the how it works

At its core, there are 3 components of the market, which are the buy-side, the sell-side, and the ad exchange / ad marketplace. For simplicity of this primer, I will leave out other enabling players such as advertising analytics players, or marketing automation players, etc. The buy-side of the industry comprises of 3 key players, which are advertisers, advertising agencies and DSPs. Meanwhile, on the sell side, there are your SSPs, publishers and your end-consumer. There is another key player within the value chain that interface with both the DSPs and the SSPs, which are the DMPs. That’s a lot to digest, but let me provide some explanation for each of them.

As reference, below are examples of the names for each of the player subsegments.

Source: Company annual report

Just to drive the point better before moving on, below is a step-by-step depiction of how you as a consumer sees an ad on a website or even on Netflix:

Ad Space Availability: When a user visits a website or uses an app (the "user" here refers to the end consumer who is browsing the internet, using apps, etc.), an opportunity to display an ad is created. This opportunity, or ad space, becomes available for advertisers to bid on.

SSP's Role: The SSP, representing the publisher's site or app, sends out a request for bids to various DSPs. This request includes information about the available ad space and the user, such as the user's location, browsing behavior, demographics, etc. This information helps advertisers target their ads effectively.

DSP's Role: When a DSP receives a bid request, it evaluates the opportunity based on the advertiser's targeting criteria and budget. If the opportunity aligns with the advertiser's goals, the DSP places a bid for the ad space on behalf of the advertiser. This happens in real-time, often in milliseconds.

Winning the Bid: Once all bids are in, the SSP selects the highest bid and grants the ad space to that advertiser. The winning ad is then served to the user's device.

Time-Bound Nature: The entire process, from the user visiting the site to the ad being displayed, is very quick, often happening in real time as the page loads. This is because the ad spaces are sold in real-time auctions, which are time-bound to the instant the user is accessing the content.

With our understanding of the digital ad market, its worth delving into which parts of the ecosystem does value accrue, and what is the potential going forward. Unfortunately, I could not find a lot of publicly listed players within some of the subsegments, such as ad exchanges and DMPs. Most of the publicly listed ones are offered by larger parent companies and these segments represent a smaller portion of their revenue such as Microsoft, Google, Adobe etc. Analysing these companies may not be a useful comparison, given that the economics do not represent the underlying segment we are interested in. Even for Google, where they generate Google Search ads, YouTube ads and even other bets. Nonetheless, there are a few pure-play publicly listed players with the advertising agency, DSPs and SSPs segments. I believe its worth delving into the economics of the publicly listed players within these subsegments, and laying over qualitative assessments on who best would be able to capture the tailwinds in the advertising industry.

Note: DSP is represented by Trade Desk, given that Trade Desk is the largest DSP in the market (aside from walled-gardens). The remaining players are relatively fragmented in the open internetand operates across different subsegments (not pureplay DSPs, which makes it hard for comparison) | Source: Company annual report, Stratosphere.io

Source: Company annual report, Stratosphere.io

Across the key players, DSP and SSPs have experienced stronger topline growth over the years, driven by the shift towards programmatic advertising. Unsurprisingly, advertising agencies have not grown significantly given that they are relatively mature companies, and are not necessarily tech-focused companies. Nonetheless, they do generate higher operating margin on average than the DSPs and the SSPs, while DSPs ROIC is higher relative to other subsegments. It should be noted that Trade Desk’s ROIC has been decreasing over the years. Much of it driven by NOPAT changes (affected by effective tax rates as well) and higher invested capital over the years. Overall, it does suggest that the economics of DSP (i.e. Trade Desk) is more attractive, relative to SSPs and ad agencies, given the relatively strong growth and attractive ROIC.

More importantly aside from the historical numbers, the question is whether this is sustainable and whether there are specific tailwinds or industry dynamics that players in each subsegment can capitalize on. I do believe advertising agencies will remain an important player in this ecosystem but will be impacted given risk of advertising functions moving in-house. I do expect growth and margins to be relatively stable as they may still be able to benefit of digitization of advertisements and may still be able to add value to customers. On the other hand, I expect both DSPs and SSPs to be the main beneficiary of continued digitalization of advertisements, coupled with a shift towards programmatic advertisement.

While forecasts vary across different research providers, its safe to say that the global digital advertising market is expected to grow at high single digits to low double digits over the coming years. Accompanying this shift is also the movement towards programmatic buying of digital ads, given the benefits from programmatic purchase of ads. Based on forecasts from Statista, global programmatic ad purchase is expected to grow at a 9% CAGR to 2026. This implies that there is underlying growth that will be beneficial for both DSPs and SSPs.

Note: (*) includes advertising that appears on desktop and laptop computers as well as mobile phone, tablet, and other internet-connected devices, and includes all the various formats of advertising on those platforms; excludes SMS, MMS and P2P messaging-based advertising. LHS from eMarketer and RHS from Statista | Source: eMarketer, Statista

Nonetheless, I believe that DSPs are able to capture more of the upside from this shift, given specific industry dynamics. The first is that it is a buyers market, given that there are more suppliers of ad inventories than there are advertisers. Secondly, is the fact that the DSP market is less fragmented than the SSP market. Trade Desk is at an advantage as a DSP given that it is the largest DSP outside of the walled-garden players, essentially the only real independent DSP. Its hard to put a number on their market share, but below is my attempt based on publicly available data that I can find (take it with a grain of salt). Based on data from Fortune Business Insight1, the global market size of the DSP market in 2022 is around USD20.76bn. This market size includes both walled gardens and open internet players. Next is to separate what is the percentage of digital ads being spent in walled gardens vs the open internet, which is approximately 77.4% and 22.6% in 20222 respectively based on data from Statista. This leads to a market size of ~USD4.7bn in 2022 and a corresponding Trade Desk market share of ~34% in the open internet[1]

This contrasts with SSPs, where it is highly fragmented in the open internet with Magnite and Pubmatic, 2 of the larger players in this space having approximate market share of less than 10% and under 5%, respectively (directional numbers based on B. Riley’s estimates). In this industry, scale is an advantage because ad agencies would naturally converge towards the largest platforms. For Trade Desk, this is beneficial due to several reasons:

Data insights: Trade Desk would have vast access to data that would allow ad agencies to target relevant audience and contribute towards better ad optimization

Access and global reach: Given its scale, Trade Desk has access to a vast array of ad exchanges and even to some publishers directly (part of their offering) globally. This would allow attract advertisers further to ensure that their ads are being placed at the most optimal spaces

Reliability and scalability: Trade Desk’s platform is highly robust (based on customer reviews) and allows ad agencies to run campaigns at scale, without performance issues

Robust integration capability: Trade Desk’s platform provides integrated access to a wide range of omnichannel inventory and data sources, and third-party services

“…on the DSP side, demand side platform, the number one you think of is the Trade Desk. The ticker on that is TTD. They are far and away the largest player in ad tech. So if you're thinking DSPs, think the Trade Desk. The other big one is Google has one called DV360.”

Dan Day, CFA, B. Riley Securities

These advantages have already materialized in the form of higher take rates by Trade Desk on ad spending relative to its SSP counterparts. Trade Desk’s take rate is approximately 20% (which includes data that they sell to their customers), while SSPs like Magnite and Pugmatic have take rates that range between 10% to 15%. These are take rates for open internet players. The problem with a fragmented market is the fact that publishers typically employ multiple SSPs (as it is highly fragmented) to broadcast their ad spaces. This creates a natural downward pressure on take rates as publishers would only choose SSPs that provide the highest price (net of take rates) for their ad spaces. Even with on-going optimization on ad spending and consolidation of SSPs, its hard to foresee SSPs, reaching the level of market share that Trade Desk has achieved. I believe that this scale will continue to be an advantage for Trade Desk as they continue to take on market share

This is a good segue into Trade Desk as a company. We are already familiar with what Trade Desk is generally. The next section will be focused on Trade Desk’s business model, specific products and services that they offer, its go-to-market strategy together with an under the hood look at their financials and economics.

Trade Desk Company Background

Overview

Trade Desk is a cloud-based programmatic ad buying platform that enables clients to plan, manage, optimize and measure digital advertising campaign. The company, initially founded in 2009 as a data management platform went public in 2016 and has since grown significantly. Trade Desk allows its clients to run ad campaigns through its platform across various ad formats, such as video, audio, display and through multiple channels (CTV, display out-of-home, mobile and desktop).

Trade Desk is specifically focused on the buy-side and represent only the advertisers and the advertising agencies. This is unlike many of the other walled garden players where they are both DSP and SSPs. Representing the buyside has its advantages. For one, it is a buyers’ market, given that digital ad spaces exceeds demand. The second advantage is that Trade Desk avoid the conflict of interest that is present when a platform serves both DSP and SSP. This focused representation allows Trade Desk to build trust with clients, which is critical to success. Clients typically use first-party data on their platform and hence are not worried that their data will be used by other participants on the other side of the advertising equation. To further ensure alignment of interest, Trade Desk also does not pre-emptively buying advertising inventory in order to resell it to the client for a profit. Instead, Trade Desk enables clients to manage their omnichannel advertising campaigns, through a self-serve platform while managing their campaign spend.

Products and Services

Fundamentally, based on their annual report, the Trade Desk platform allows ad agencies to do the following:

purchase digital media programmatically on various media exchanges and sell-side platforms;

acquire and use third-party data to optimize and measure digital advertising campaigns;

integrate and deploy their proprietary first-party data within our platform to optimize campaign efficacy;

monitor and manage ongoing digital advertising campaigns on a real-time basis;

link digital campaigns to offline sales results or other business objectives;

access other services such as our data management platform and publisher management platform marketplace; and

use our user interface and APIs to customize and expand platform functionality.

These functions are further supported by key new features such as:

Koa Artificial Intelligence. Koa, their predictive algorithmic tools that help platform users make data-driven decisions without sacrificing control or transparency, makes recommendations for campaign optimizations based on its sophisticated analysis of rich data sets. Advertisers can then choose which optimizations make the most sense for their campaigns.

Kokai: Distributes the power of Koa’s AI across various aspects of media buying on The Trade Desk platform. This includes predictive clearing, which ensures traders make bids at the optimal level; scoring every ad impression based on relevance to the advertiser; upgrading measurement and forecasting; increasing resilience, even in the absence of identifiers; budget optimization; and KPI scoring.

OpenPath: establishes a direct connection between The Trade Desk’s clients (advertisers and agencies) and premium digital publishers. This approach bypasses traditional intermediaries in the programmatic ad buying chain, like Supply-Side Platforms (SSPs).

UID 2.0 (Unified ID 2.0): Given the move from Google to eradicate 3rd party cookies, Trade Desk has been at the forefront of creating a new approach towards user identity in the context of advertising. UID is an open source, interoperable identity framework. It uses encrypted, anonymized, user-specific IDs, which are created with user consent.

At the core of its platform is the bid-factor-based architecture that allows users to define desirable factors and the value associated with those factors. Based on these factors, the platform can compute the value of impressions in real time and bid only for optimal impressions. Because of the granularity of the bid factors, clients can rapidly create billions of different bid permutations with only a few clicks. This expressiveness enables better targeting, pricing and campaign results.

Without getting too technical, within programmatic advertising, there are 2 methods of running ad campaigns which are line item vs bid-factor architecture. The key thing to remember is that bid-factor architecture is more dynamic and offers more granularity and flexibility for advertisers in running their ads (more on the difference in the appendix), which in turn improves their ability to adjust and optimize for better ad performance.

Client base and GTM Strategy

Trade Desk’s clients are actually the ad agencies that represent the advertisers. As of 2022, Trade Desk has over 1,000 clients, consisting primarily of advertising agencies or groups within advertising agencies that have independent relationships with Trade Desk. Trade Desk would sign Master Service Agreements (MSAs) with these ad agencies to provide access to users to use the Trade Desk platform. These MSAs do not contain material commitments on behalf of clients to use our platform to purchase ad inventory, data or other features and have 1 year terms, which automatically renew for 1 more year unless stated otherwise. What has been impressive is their customer retention which has been consistent at 95% since 2014.

Trade Desk has also begun to develop multi-year joint innovation partnerships (JVPs) with ad agencies and advertisers as highlighted in their 3rd quarter earnings call. JVPs are a multi-year commitment between ad agencies and Trade Desk, which includes a level of commitment to spend on Trade Desk platform. The largest JVP signed this year represent a future annual spend of USD1bn per partnership. The move towards mutli-year partnerships has also been more prominent this year.

“…agencies and advertisers are increasingly shifting more of their campaign dollars to decision, data-driven opportunities, where they can have more confidence that those dollars are working as hard as possible.”

Jeffrey Green, CEO of Trade Desk, Q2 2023 Earnings Call

While their client base are ad agencies, partnerships doesn’t just stop there and are also encroaching the supply side of the ad ecosystem. To date, Trade Desk has also been proactive in reaching out to connected TV (CTV) players such as Disney in order to capitalize on the secular adoption of streaming services, with an ad-tier subscription. These partnerships are critical in order to ensure that advertisers will keep on relying on Trade Desk to run their ad campaigns amongst the CTV players. They have also formed partnerships with retail players such as Walmart, where multiple advertisers are also placing ads through Walmart, with Trade Desk’s support.

Revenue Model, Financials and Operating Metrics

Trade Desk primarily generates its revenue from charging customers a percentage of their ad spend on the platform. In addition to that they also charge customers for additional data sets and services. That being said, it is relatively simple to breakout the revenue drivers of Trade Desk, which are i) Number of customers (taking into account churn), ii) Average spend per customer and finally iii) Take rate by Trade Desk.

Since 2014, gross spend on the platform and revenue has grown at a staggering 54% and 41% CAGR, respectively. Meanwhile, take rates on the platform has hovered around 20% over the years. Meanwhile, gross billings, which is gross spend net of platform discounts and the value of advertising inventory and data that clients purchase directly from publishers through the platform has also grown at an impressive rate.

Source: Company annual report

Part of this growth has of course been driven net addition of clients over the years from 258 in 2014 to over 1,000 in 2022. Nonetheless, the rate at which client base grew has dwindled in recent years. I think partly is because there is only so many ad agencies there are in this world, that are big enough. Trade Desk has already captured the largest ad agencies in the world such as Publicis Groupe WPP etc, which represent the Ad Age top 200 advertisers and majority of the S&P 500 companies. As a result, client acquisition going forward will be targeted on the smaller players, and may not necessarily be strong drivers of growth going forward.

Trade Desk is also one of the rare high-growth tech companies that has achieved profitability, even on a net income basis, which is an impressive feat. Below is a summary of Trade Desk’s income statement. Margins have improved over the years despite some volatility. Unsurprisingly, the company generates significant amounts of cash each year, and barely has any debt on its balance sheet except for some operating leases.

Source: Company annual reports, Stratosphere.io

Setup of the stock today

After its 3rd quarter earnings results, Trade Desk’s share price fell by 30% (but has recovered some of the losses). The company beat its revenue, EPS, and EBITDA consensus estimates for the quarter. Earnings per share came out at 33 cents, adjusted vs. 29 cents expected by analysts while revenue came out at $493 million vs. $487.04 million expected by analyst. It was a solid quarter overall, generating USD200m adjusted EBITDA vs guidance of USD185m for the quarter. Nonetheless, the company provided a lower-than-expected guidance for Q4, at USD580m vs USD610m expected by analyst (lower by ~5%). The lower guidance primarily came from the fact that they saw more macroeconomic uncertainty at the start of Q4, as they some weakness from certain verticals such as automotive.

“So that said, starting about the second week of October, we began to see some transitory cautiousness around certain advertisers. For example, we saw some reduction in brand spend in verticals such as automotive and consumer electronics, for instance, specifically around cell phones and media and entertainment. Some of these industries have been recently impacted by strikes such as the U.S. auto industry. So the first week in November, we have seen spend stabilize and we're very confident that we will continue to outpace our industry and gain market share”

Jeffrey Green, CEO of Trade Desk, Q3 2023 Earnings Call

The question then is, is the market reaction justified? Potentially. The fact is Trade Desk trades at a really high multiple, relative to other ad players or tech companies and this has always been the case historically. They are essentially priced to perfection and so a disappointing guidance can surely cause a violent share price movement. As compared to its tech peers, TTD is also relatively overvalued, trading at ~40x EV/ NTM EBITDA and 15x EV/ NTM Sales.

Source: Koyfin

At its current price, a reverse DCF would suggest that market is expecting continued growth above 20% even in to 2030 with a NOPAT margin of 21% by 2030. These are lofty numbers I am not going to lie. Even after the sell-off the stock is still trading at a high multiple relative to other tech peers. But I believe these valuations are justified just given the fundamentals of the business. I doubt we will ever find TTD cheap enough or be undervalued relative to tech peers and so as an investor, it is more the question of when you enter.

Source: own estimates

I believe that Trade Desk can trade at $190 over the next 5 years, which would imply a return of ~177%, from the current price. Much of my thesis will be driven by top line and EBITDA growth while maintaining relatively conservative assumptions on multiples for Trade Desk expanding from 31x EV/ Adj. EBITDA to 36 by 2028.

Primary Investment Thesis

TLDR:

Macro tailwinds is being captured effectively by Trade Desk

Shift towards CTV

Retail advertising

Balance in budget between walled gardens and open internet

Strong competitive moat as evidenced by solid economics, sticky business model, and customer preference

Trade Desk is investing in improving its platform and investing in client acquisition and relationships despite the macroeconomic uncertainty. This will lead to an acceleration of revenue as the economy recovers.

Macro tailwinds

Inevitably, growth within this space is highly impacted by new innovations in adjacent industries. The proliferation of smartphones and social media led to an increase in mobile ads, increased internet bandwidth led to proliferation of video ads and many others. This is one of the core attractiveness of companies within this space, which is a direct beneficiary of new technological innovations, assuming of course the company invests in these new growth vectors. There are multiple lenses to consider when looking at what macro factors will impact Trade Desk’s ability to grow. I believe there are 3 to consider:

Channel mix i.e. which channels will grow the fastest, and is Trade Desk in the right position to capture these benefits.

Adoption of digital platforms: i.e. social media, e-commerce platforms, fast / instant delivery platforms, or any new platforms that will rely on ad revenues as a core part of their business model

Allocation of digital ad budget between walled gardens vs open internet: i.e. will advertisers increase their budget within open internet or walled gardens further?

From the 3 factors above, we are seeing CTV as one of the fastest growing channels in terms of user adoption. Adoption of digital platforms are continuously increasing, with more users using services like Instacart or e-commerce platforms. Lastly, the potential for a shift in budget allocation towards open internet vs walled gardens.

Shift towards CTV

For a brief background, CTV is essentially, televisions that are connected to the internet either through streaming boxes, gaming consoles or smart TV sticks (e.g. Roku, Apple TV etc). CTV has grown significantly over the years, a proxy of such a movement can be seen from the increase in proportion of US households that are subscribed to linear TV over the years, and this number is expected to decrease over the years. It should be noted that I don’t think linear TV will completely die and some households may have both CTV and linear TV together. But the trend does suggest that CTV will gain prominence across the world. Rise of subscribers from Netflix is also a good proxy of this movement. Given this shift, it is unsurprising that advertisers are increasingly allocating more ad budgets to CTV and less towards linear TV. The shift towards CTV is not only driven by a secular shift on the demand side but also from the supply side. Advertisers are increasingly interested in measuring the returns on their ad placements. The ability to track various metrics and offer better personalization to the viewers in terms of ads being shown is leaps and bounds ahead for CTV relative to linear TV. Ad placements in linear TV is generic and based on insertion orders, which reduces the ability for advertisers to target audiences.

Source: eMarketer

In addition to the shift towards CTV, the more important shift is of course a shift towards programmatic purchase of ads, in which not all players have embraced. Not all premium video content companies have fully embraced programmatic buying (as highlighted in their Q3 2023 earnings call), which they will eventually. Their Q3 call shed a light on how this dynamic will play out, and I do agree with management on this.

“In order to get incremental subscribers, they can't simply keep raising prices. Some consumers would rather spend a few extra minutes, considering ads they watch than pay more for subscriptions. High-priced subscriptions alone will not provide the incremental subscribers media companies need to continue growing.

As recently reported by Hollywood Reporter and I quote, "Executives at every major streaming giant with both an ad-supported and an ad-free tier, including Disney, Netflix, Paramount, Warner Bros. Discovery and NBCU say that the total revenue per user is higher on the ad-supported plan than it is on the ad-free plan." Not only do media companies generate more revenue per user within an ad-supported option but the potential for growth is much greater. Ultimately, there's a limit to how much viewers will spend on subscriptions. Economic pressures on the consumer right now are increasing the appeal of a free or low-cost option that is supported by ads.

However, this model is only sustainable if the ad load is significantly lower than traditional linear television. And the only way we get there is if the ads are relevant to the viewer so that the advertisers are willing to pay more for each of them.”

Jeffrey Green, CEO of Trade Desk, Q3 2023 Earnings Call

Trade Desk has been able to capture this shift quite well. It has introduced various new product such as OpenPath, which allows advertisers to secure premium ad inventories directly with the publishers, or in this case, the premium content providers themselves. OpenPath improves transparency for advertisers, allows for direct access to premium ad inventory. Its TV Quality Index also showcases the value of premium TV content over UGC platforms. These innovations have clearly driven platforms to open up more of their premium inventory to Trade Desk. Disney has opened up its Disney+ inventory across Europe. Many providers are also opening up more live sports inventory, perhaps the crown jewel for most streaming providers for programmatic buying on Trade Desk’s platform, with billions of avails every single week. I expect this to continue going forward, providing a solid baseline of growth for Trade Desk.

One call option on this is the potential partnership with Netflix, the largest streaming provider of all. At the moment, Netflix is partnering with Microsoft to run its ads on Netflix, but this partnership is set for renewal next year. I believe that Trade Desk has the opportunity to win and become a partner for Netflix, providing access to ~247million subscribers for advertisers. There are already rumours of Netflix’s partnership with Microsoft not being in the best position. Of course Netflix, can in the end decide to build it on its own, but I believe partnering with Trade Desk may be the best option given the scale that Trade Desk in representing all the top advertisers in the world, together with Trade Desk’s technology to drive better programmatic buying on Netflix. Trade Desk’s track record speaks for itself.

Rise of retail advertising given higher digital retail platform adoption

On retail advertising, Trade Desk has partnered with many major retailers such as Walmart and Albertsons, by allowing advertisers to have access to data owned by these retailers. This will allow better targeting by advertisers within ad spaces provided by these major retailers. Similarly, Walmart has also been partnering with digital first e-commerce platforms such as Instacart in the US and Tokopedia in Asia. These partnerships will prove to be useful as e-commerce sales will represent a larger portion of retail spending globally, signifying more opportunities for advertisers to advertise through these e-commerce platforms. By activating retailer’s data, advertisers are able to measure with more precision how their ad dollars are spent and what are the returns from it across the funnel.

Source: Statista

Potential shift in budget for open internet vs walled garden

The final part of the equation is this shift in budget. Its tough to put a pin on this to forecast what the budget allocation would look like for open internet vs walled garden and so I think I would bucket this as a call option as well. Statista forecasts that walled gardens share of global digital advertising revenue will continue to increase to 2026, from 77.4% to 82.4%. On the flipside, Trade Desk believes that open internet will gain in prominence (no shit because they need this to happen) going forward. Nonetheless, it would be useful to understand how this dynamic can shift. Walled gardens are notorious for their lack of transparency on their data. This leads to some sort of a black box for advertisers when they decide to place ads on these players. The benefits however are high, given that these players have significant reach towards audience, with deep understanding on user behaviour. While targeting is done proprietarily, the ROI from these platforms are commendable. So how should we think about it? Lets look at the data. Undeniably, number of social media users have increased over time, standing at 4.95bn globally as of October 2023, from 4.5bn in October 2021 and consequently the importance of walled gardens within the digital ad space. More importantly, as 3rd party cookies will be displaced in 2024, it makes sense for advertisers to lean in on walled garden players given the richness of data that they possess, robust vendor ecosystem and many others.

On the flipside, one can argue that the removal of 3rd party cookies mean that there are more reliance from advertisers for their 1st party data and also 3rd party data from DMPs, that can be easily integrated, which is where Trade Desk fits in perfectly. Based on a survey in 2020 (though slightly outdated), internet users in the US actually spend 60% of their time in open internet platforms, but ad spend on open internet is only at 40%. A similar but more recent study from Trade Desk (as of 18 November 2023, take it with a grain of salt), suggests the same as well. It is also important to note that ad effectiveness, is also relatively high in the open internet compared to walled garden platforms, which is definitely unexpected. Given the macroeconomic uncertainty, I believe ad dollars will shift towards mediums that offer the greatest ROI. As such, despite the importance of walled gardens for digital ad placements, I would not be surprised if the tide moves against them and advertisers begin to increase some ad spending allocation towards the open internet.

Source: Trade Desk, Statista

Strong competitive moat and defensibility

If I think about what makes Trade Desk a leading company, I can think of 3 main things. I think these 3 factors will continue to drive better performance for Trade Desk going forward.

Scale

Network effects

High switching cost

Trade Desk is without a doubt the largest DSP in the open internet, with an estimated ~34% market share within the DSP segment from my back of the envelope calculation. As mentioned previously, scale is highly important to get access to premium ad inventory. This is increasingly more important to advertisers given that they need to be able to blast their ad campaigns at scale, in the most efficient way (it needs to be at scale, cost-efficient and effective). Trade Desk is also able to analyze significant amounts of data and be able to utilize it for better ad performance and also ability to run digital ad campaigns at scale reliably.

I believe as a business Trade Desk has its own network effect at play, which leads a flywheel effect. Given its scale, Trade Desk already represents most if not all the top advertisers in the world. SSPs and ad exchanges would want to establish relationships with Trade Desk given the massive representation of advertisers. Trade Desk already obtains ad inventories from over 100 SSPs and ad exchanges. In addition to this relationship, multitudes of publishers / content platform outside of the would also to also use Trade Desk for direct ad placements (through OpenPath) given that the large base of advertisers would pay top ad dollar for premium inventory. We have already seen them partnering with CTV, retail players and even digital first e-commerce platforms such as GoTo and Instacart. More ad inventories would then increase attractiveness of the platform for advertisers, hence creating this flywheel effect, where they are more willing to spend on the platform. This is evident by the JVPs that Trade Desk has been signing for multi-year partnerships and billions in spending commitment. What is important to note is also the fact that Trade Desk is already disrupting the SSPs, through its OpenPath product as it removes the need for intermediary.

The final part of the defensibility of the business is the high switching cost that the platform has, despite being a self-serving platform. The platform is easy to use and customizable through their API. The platform’s UX is easy to use, allowing for ease of use even if users are not used to the platform. The second is their ability to integration with other services relative to other DSPs. As more advertisers integrate with the Trade Desk platform, it inevitably increases the stickiness of the platform. The last thing is of course the exceptional customer service that they provide. All these components incrementally increase switching cost for clients.

“Integrations - TTD is ahead of the curve in terms of integrations with other services compared to other DSPs (ex. Attain, Placed/Foursquare, Roundel) Product Roadmap - TTD is also ahead of the curve in terms of betas/cookieless solutions - UID2.0 Customer Service - same as above, top notch customer service with the team always willing to help in terms of troubleshooting/strategizing”

TTD Customer, Associate Director of Media Company (<USD50m revenue), Gartner

Continued expansion despite macroeconomic uncertainty

Listening to their Q3 call, Trade Desk is clearly in investment mode, to capture further market share in these uncertain times. This is exactly what you would like to see from a company, with a strong balance sheet and cash flow generation capabilities.

The company is pushing for better innovation, investing in secular trends, international market expansion and investing in human capital. Trade Desk has been very proactive in driving innovation in the space, through its introduction of UID2.0 as a safer more transparent alternative to 3rd party cookies, the development of Open Path, to reflect publishers’ demand to sell their premium ad spaces and also in AI through Koa and Kokai. All these innovations will inevitably improve its product offerings to clients, drive better retention and at the end of the day mode ad dollars pushing through the platform.

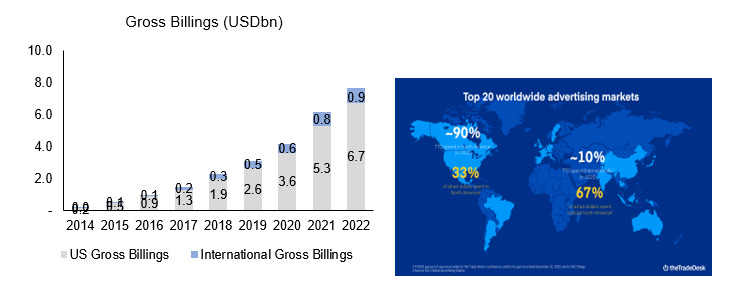

As noted above, the company is investing heavily in CTV and retail media, which are clearly the right places to invest in. I believe they are well placed to benefit from the ongoing shift and it doesn’t seem likely that other players can displace them in the open internet. On top of investing in the right channel mix and partnerships, they have also been focused on expanding internationally. Its gross billings from international markets, have grown at an impressive rate of 54% CAGR since 2014 to 2022 but represents only 12% of its overall gross billings. In terms of potential upside, 67% of global ad spending is done outside of North America (as of 2022), which implies significant upside for Trade Desk.

Source: Company annual reports, investor presentation

The final investment I would like to highlight is the fact that they are continuously investing in their team capabilities and capacities. In the Q3 call, the CFO highlighted that they were increasing headcount by 15-17% this year and next year. Tough to say if this is significant or not, but undoubtedly a sign that they are willing to be aggressive to push for better market share gain. On top of that, these investments are focused on productivity with their engineering teams, go-to-market teams, sales, account management and trading.

“You bet. So implicit in the question is that, hey, when -- as the macro continues to improve, where will you make additional investments? We're investing as aggressively as we can right now. So I know we're sort of showing our operating leverage but that's not because we're saying let's flex our operating leverage. We're instead trying to grow as aggressively as we can. But as Laura highlighted in the change in headcount both this year and next year as it relates to our overall growth, that's in part because we surged our hiring during the pandemic and over the last few years so that we could capture opportunities like this one, including that we're shipping the biggest release in the history of the company this year.”

Jeffrey Green, CEO of Trade Desk, Q3 2023 Earnings Call

Valuation and risks

So where does this all land in terms of valuing Trade Desk? I contemplated a lot on how best to model Trade Desk particularly its topline revenue driver, which is the key part to get right for a high growth company like Trade Desk. 2 methods to do this:

Bottom-up revenue driver: The benefit of this approach is that I get to model potential client acquisition, churn rate. Take rates and average spending per client and see how each of these levers would progress over time. I believe bulk of the driver would come from higher average spending per customer, given the innovation and investment in capabilities that they have done.

Top-down revenue driver based on markets: This approach allows me to model the nuances between US and international markets, given that one of the main growth drivers is international expansion. This method would require making some assumptions on market size of the DSP market and how it is expected to grow going forward.

I think it makes sense to use a bottom-up revenue driver as primary method to model growth for Trade Desk, and sense check the numbers through the second approach. Based on my estimates, which arguably can be lofty, I believe revenue growth will likely accelerate after 2024, as the economy and ad spending stabilizes. On top of that, I believe, that will be able to incentive higher gross spend on their platform given their continuous innovation, into 2026 before growth tapers down. Meanwhile I am also estimating that OPEX will as a percent of revenue will come down as the company scales, leading to lower S&M, R&D and G&A spend. Meanwhile, I expect there to be some multiples expansion, which I believe is still conservative given where Trade Desk typically trades. Below is a summary of my valuation. The one caveat is that I am worried I am underestimating the share count dilution (which I am currently just growing at recent historical rates), with SBCs increasing in value. If any of you can help with how best to model dilution, let me know!

Source: Own estimates

In addition to the above, I also sense checked the numbers by overlaying the implied market share analysis for Trade Desk, using Fortune Business Insights’ numbers. These assumptions are highly directional but gives a sense of how realistic this growth rate for Trade Desk that I am projecting. By 2027, Trade Desk is expected to achieve a market share of 55% in the open internet DSP market, which I believe is highly likely.

Source: Fortune Business Insights, Statista, Own estimates

Risks are more external compared to business fundamentals

I believe key risks for Trade Desk are more macro rather than business-specific factors. A few things that are top of mind for me. The first is whether there will be continued demand and need for partnerships by premium content providers with Trade Desk. Essentially, can Trade Desk continue to ride the CTV wave and become a preferred player to partner with. The decision to build in-house vs using Trade Desk, is a key risk for Trade Desk. While all datapoints today indicate that these providers are better off working with Trade Desk, it is still a risk in the future.

The second risk is continued adoption or importance of open internet for digital advertising as I have initially highlighted above. 2 sides of the argument, driven by the increasing demand by advertisers to be as efficient as possible in terms of allocating ad dollars. As purchasing decision are increasingly driven by social factors and further reinforced through social media platforms, who they themselves have been investing in social retail, it is a risk that ad dollars would increasingly be allocated to these platforms (i.e. walled garden players). On the flipside, data has also shown that open internet can be as effective and even more effective in targeting audiences and driving high ROI on ad dollars. This is a tough call, but I am leaning towards both being important going forward and will have a role within the digital ad space and ad budgets will continue to be allocated to both as well. Given the demand for higher transparency and ability to measure to the highest level of detail, and integrate with first party data, I do believe DSPs in the open internet, and particularly Trade Desk will continue being important. Evidence has shown so far, how much advertisers are willing to spend on the platform and the multiple levels of partnership being formed. I do believe this will continue going forward.

The third risk is of course valuation. Valuation has always been high for Trade Desk, but this has compressed drastically over the past 2 years. Nonetheless, this is still high relative to other Tech peers. The risk of it coming down is there as with any high growth companies.

Source: Stratosphere.io

Concluding thoughts

This was a long essay and so thanks for those who read it. Its much a learning for me as I would hope for you too. I hope this essay gives a comprehensive view of how the digital ad ecosystem works and why Trade Desk is best positioned to capitalize on the secular trends impacting the industry.

I am still trying to improve my thinking process and making things more succinct. Translating qualitative insights into numbers, and also improving on how best to model company fundamentals and even the details of modelling line items. Please share any feedback that you have!

Disclaimer - This article is not advice to buy or sell the mentioned securities, it is purely for informational purposes. While I’ve aimed to use accurate and reliable information in writing this, it cannot be guaranteed that all information used is of such nature. The views expressed in this article may change over time without giving notice. The mentioned securities’ future performances remain uncertain, with both upside as well as downside scenarios possible. Before making any investment, it is recommended to speak to a financial adviser who can take into account your personal risk profile.

[1] Another method, is to take a cut of global programmatic ad spending from the figure above, but I believe the market definition for programmatic ad spending includes marketing automation as well, together with other segments including SSPs.

Sources

1Programmatic advertising worldwide - statistics & facts | Statista

2Worldwide Digital Ad Spending 2023 - Insider Intelligence Trends, Forecasts & Statistics

3https://www.fortunebusinessinsights.com/demand-side-platform-dsp-market-104793

4Walled gardens share of digital ad revenue 2027 | Statista

TV and Connected TV Ad Spending Forecasts 2023 - Insider Intelligence Trends, Forecasts & Statistics

Reasons for shifting ad spend to CTV/OTT U.S. 2023 | Statista

Netflix rehauls advertising partnership with Microsoft, slashes prices - OnMSFT.com

Global e-commerce share of retail sales 2027 | Statista

What the end of third-party cookies means for advertisers (deloittedigital.com)

https://datareportal.com/reports/digital-2023-october-global-statshot